Ireland’s property market has always been a topic of hot debate, especially considering its rollercoaster history from the Celtic Tiger boom to the subsequent property bubble burst.

For investors, the market’s direction in 2025 might hinge on several factors: the actual impact of interest rate adjustments, the ongoing effects of government policies aimed at cooling speculative buying, and the global economic climate. For home buyers, particularly first-timers, navigating this market requires a careful balance between leveraging government support and timing their entry to avoid the peak of what could be another cycle of overvaluation if current trends continue unchecked.

This analysis not only underscores the complexity of the current Irish property market but also emphasizes the need for nuanced understanding beyond the headlines, considering both policy impacts and market psychology in shaping future outcomes.

Market Sentiment and Price Dynamics:

The data would indicate a robust growth in property prices, with a year-on-year increase of nearly 10% nationally as of July 2024. This surge, particularly evident in Dublin where prices have jumped by over 10%, reflects not just a recovery but a market that has surpassed previous peaks set during the Celtic Tiger era.

However, this growth comes amidst concerns over sustainability, with supply struggling to keep pace with demand, leading to what some might call a ‘panic buying’ scenario driven by Fear Of Missing Out (FOMO).

Investment Climate:

The sentiment among investors shows a mix of optimism and caution. Interest rate cuts anticipated by the end of 2024 could stimulate market activity further, making borrowing cheaper and potentially inflating property values even more.

However, the introduction of measures like the 10% stamp duty on bulk purchases has cooled the market for institutional investors, or so-called ‘vulture funds’, aiming to level the playing field for individual home buyers. Yet, this has also led to unintended consequences, with reports suggesting that rent controls and such policies might be deterring much-needed foreign investment in residential real estate.

Supply and Demand Mismatch:

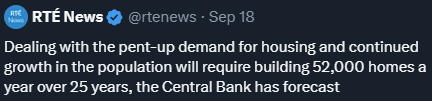

The ongoing issue of housing supply remains critical. Despite the demand for approximately 52,000 new homes annually, construction has not matched this need, with projections suggesting a decline in homebuilding in 2024 compared to the previous year.

This deficit, estimated at about 250,000 homes, continues to exert upward pressure on both rental and purchase prices, making affordability a central concern for potential homebuyers.

Government Interventions and Their Impact:

Government schemes like Help to Buy and the First Home Scheme continue to play a pivotal role in supporting first-time buyers, particularly for new builds. However, the effectiveness of these initiatives in truly easing access to homeownership amidst rising costs and economic pressures remains under scrutiny.

Moreover, the extension of such schemes signals government recognition of the ongoing crisis but also highlights the reliance on policy interventions to keep the market accessible.

Current Market Dynamics:

- Price Trends: As of late 2024, Ireland has seen property prices surpass the 2007 peak, with significant growth particularly in Dublin and the commuter belt. This resurgence is driven by a combination of economic recovery, high demand, and a still-recovering supply chain for new builds.

- Demand vs. Supply: Despite initiatives like the Help-to-Buy scheme and changes in borrowing regulations, the supply of housing still lags behind demand. This imbalance continues to push prices upward, although at a potentially slower rate than in the past three years.

- Legislative Impact: Recent government interventions, like the stamp duty on bulk purchases, aim to curb investor purchases and favor individual home buyers, yet the effectiveness of these measures is under scrutiny.

Future Outlook:

- Price Stabilization: Analysts from X posts and broader market analysis suggest that while significant dips are not expected in the immediate future, the rate of increase might stabilize due to increased supply and regulatory adjustments.

- Investment Opportunities: For investors, the rental market remains lucrative due to high demand, especially in urban areas. However, they must navigate increased regulation and taxation aimed at protecting home buyers.

- Home Buyers: The market remains challenging for first-time buyers, with affordability being a significant issue. However, government schemes and a potential increase in new builds could ease entry into the market.

Strategic Considerations:

For Investors:

- Diversification: Consider areas outside of Dublin where growth potential might be higher due to lower initial prices and increasing demand as remote work becomes more normalized.

- Long-Term Rentals: With the complexities in rent legislation, focusing on long-term rental strategies could provide stable income while navigating less through the regulatory landscape.

- Development Opportunities: Investing in developments or renovations could offer value, especially with schemes like the First Home Scheme supporting new builds.

For Home Buyers:

- Timing and Schemes: Utilize government schemes like Help-to-Buy for new properties. Also, keep an eye on policy shifts that might make borrowing easier or more advantageous.

- Location Flexibility: Considering commuter towns or less central areas might offer better affordability and value for money, especially as infrastructure improves.

- Future Proofing: Look for properties that will remain desirable – good transport links, local amenities, and potential for home office space.

The Need For Caution:

A broader market analyses, reflects a mixed bag of caution and optimism regarding real estate markets, including the Irish property market. There’s a palpable caution about potential downturns due to several factors like rising interest rates, which traditionally dampen housing demand by making mortgages more expensive.

Furthermore, the phenomenon of homeowners locked into lower mortgage rates contributes to a reduced supply of homes for sale, potentially staving off a significant price drop but also stagnating market fluidity. On the flip side, some optimism stems from the expectation that interest rate cuts could revitalize the market, alongside interest from overseas investors looking for opportunities in potentially undervalued markets.

However, even with these positive notes, the overall sentiment leans towards caution, with concerns over economic stability, the sustainability of housing prices, and the broader implications of a market where first-time buyers find entry increasingly difficult due to affordability constraints. This duality suggests a market at a potential inflection point, where both a downturn and a stabilization could be on the horizon, depending on myriad domestic and global economic factors.

The Irish property market presents a landscape filled with both challenges and opportunities. For investors, the key is in understanding the regulatory environment and focusing on sustainable rental yields or strategic property development.

For home buyers, patience, flexibility on location, and leveraging government support can pave the way to homeownership.

Success in this market demands a proactive approach. As we look towards the future, the market might see a stabilization in growth rates, making it essential for both investors and buyers to stay informed and adaptable.

Remember, property investment, like any investment, carries risk, but with careful strategy, the Irish market can still offer substantial rewards.

In Summary:

- Economic Context: Ireland’s property market has been influenced by the aftermath of the Celtic Tiger era and the subsequent economic downturn post-2008, which saw a property bubble burst leading to significant economic and banking sector challenges.

- Market Stabilization: Recent analyses, like the SCSI report, indicate a stabilization in property prices with only a modest increase forecasted for 2024. This stabilization comes after a period of rapid price increases, now slowed by various economic factors, including higher interest rates.

- Government Involvement: The Irish government has become heavily involved in the housing market, with estimates suggesting that up to 50% of new housing completions in 2023 had some form of state influence. This involvement aims at addressing the housing crisis through direct action or financing, particularly in an election year where housing becomes a pivotal issue.

- Affordability and Supply: Despite stabilization, affordability remains a significant issue, especially in areas like Dublin. The supply of new homes continues to lag behind demand, which has intensified due to underestimated migration figures and overall population growth.

- Policy Measures: To aid affordability, the government introduced tax credits, and there’s a focus on increasing housing supply through various initiatives. However, there’s a debate on the effectiveness of these policies, indicating criticism over policies like negative gearing, capital gains tax discounts, and the lack of control over foreign investment in property, which critics argue inflates the market.

- Regulatory and Market Adjustments: There’s an ongoing discussion about the need for regulatory changes to prevent market distortions, like limiting tax incentives for property investments or adjusting policies to encourage new builds over purchasing existing stock.

- Future Outlook: The market is at a point where government policy will significantly dictate future trends. There’s an expectation for policies to adapt, potentially focusing on sustainable building practices, increased public housing, and possibly adjusting tax treatments to cool down investment-driven purchases.

Disclaimer: The information provided here does not constitute investment advice or a guarantee of performance. Investing involves risks, including the possible loss of capital. Seek advice from financial and tax professionals tailored to your financial circumstances and goals.